First-time homebuyer ? .. There are some rules

Here’s how “first-time homebuyer” is

defined across three major programs Canadians often rely on: the Ontario

Land Transfer Tax Rebate, the RRSP Home Buyers’ Plan (HBP), and the

First Home Savings Account (FHSA).

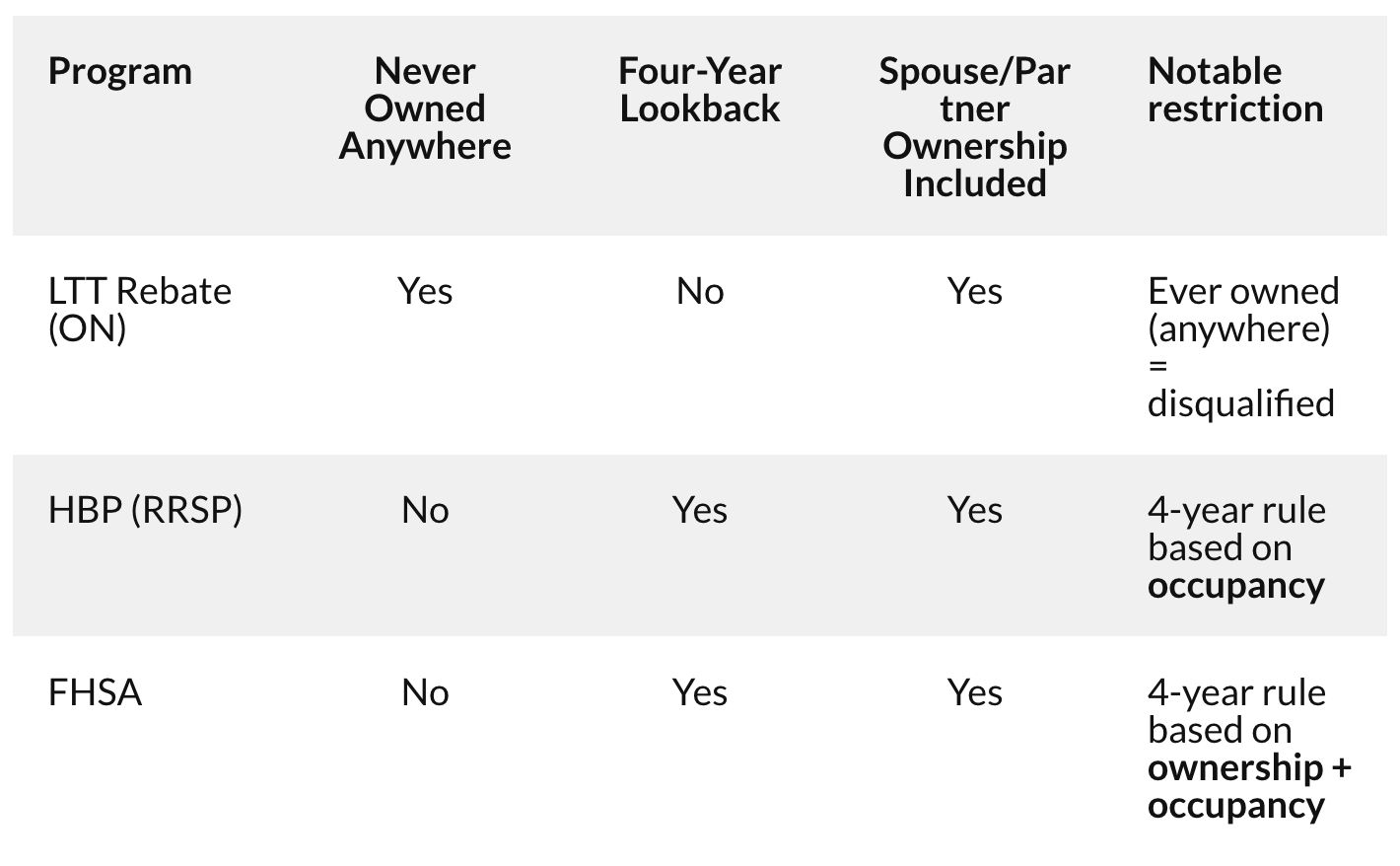

If you’re buying property in Ontario, the land transfer tax (LTT) rebate is probably the first program you’ll hear about. It can save you up to $4,000 on the provincial land transfer tax, and another $4,475 on the Toronto municipal land transfer tax if you’re buying in the city.

But the eligibility rules here are strict:

- You must be at least 18 years old

- You must have never owned a home or any interest in a home anywhere in the world

- You must live in the home as your principal residence within nine months of the purchase

- And, here’s the kicker, your spouse or common-law partner must also never have owned a home while you’ve been together

The HBP is a popular option for buyers who want to tap into their RRSP savings, up to $60,000 per couple, to help with a down payment.

Thankfully, this program is more forgiving than the LTT rebate:

- You must not have lived in a home that you (or your spouse/common-law partner) owned in the current year or the four preceding calendar years

- You need a signed agreement to buy or build a qualifying home

- You must intend to make that home your principal residence within one year

- You must be a resident of Canada at the time of the withdrawal and when you buy the home

The FHSA is the new kid on the block, and honestly, it’s a game-changer. It combines the tax perks of an RRSP and a TFSA, and lets you contribute up to $40,000 toward your first home purchase.

Similar to HBP, but tied to ownership and occupancy:

- You must be between 18 and 71 years old and a Canadian resident

- You must not have owned or jointly owned, or lived in, a qualifying home in the calendar year before you open the FHSA or during the previous four calendar years

- This rule also considers property owned by your spouse or common-law partner that you lived in

The key takeaway? The LTT rebate is the strictest. HBP and FHSA are more flexible, especially if you’ve taken a break from homeownership or recently separated from a partner who had a home.